Do your employees know the implications of naming a dependent with special needs as a beneficiary — or what happens if they don’t name a beneficiary at all?

Helping employees understand the beneficiary basics ensures their insurance policy benefits, retirement account assets, and Health Savings Account (“HSA”) (established with high deductible medical plans) funds go to the right people if the employee passes away.

Given life insurers paid out more than $88 billion in death benefits in 2022, this is no small matter.1 Encouraging employees to review and update their beneficiary information regularly can also help relieve busy HR staff workloads.

Doing so encourages the claims and distribution processes to run smoothly, providing employees’ loved ones with timely access to the benefits and support they may need during a difficult time.

Understanding beneficiary choices

When it comes to designating beneficiaries, details are key. You want to ensure employees understand how the beneficiary process works, why keeping beneficiary information updated is essential, and what’s at stake if no beneficiaries are named.

Primary Beneficiary: The first choice — or primary beneficiary — can be one person or multiple people. They are first in line to receive an insurance policy death benefit, or the funds held within a retirement account or HSA. The percentage interests of all primary beneficiaries must add up to 100%. For married employees with a 401(k), their spouse is the sole primary beneficiary by default, unless a spousal consent form is signed waiving this right. This rule can also apply to HSAs.

Contingent Beneficiary: Secondary or contingent beneficiaries will receive the death benefit, retirement, or HSA funds if the primary beneficiary/beneficiaries don’t qualify as a beneficiary under the policy or have already passed away. The percentage interests of all contingent beneficiaries must add up to 100%.

None of the above: If employees don’t name an account beneficiary, there are a few possible routes for death benefits or account funds:

- The proceeds may go to the deceased’s estate.

- A probate court may decide who will receive the funds, per the deceased’s will, if there is one. It’s worth noting that the probate process can be lengthy.

- A pre-determined order of beneficiaries may be used to determine who receives the funds. The death benefit will be paid as outlined in the certificate of coverage or governing plan documents. As an example, the benefit payment order may start with the spouse, then move on to children — or proceeds could be paid to the estate.

Either way, if employees don’t name their beneficiaries, or have a will, they don’t get to decide who receives their assets.

An important consideration

The circumstances of beneficiaries can also make receiving benefits or assets more complicated. As employees contemplate whom they’d like to receive their death benefits and account assets, they should consider the following:

- If they want to name someone with special needs as a beneficiary: If employees have dependents with special needs, they may understandably wish to designate them as beneficiaries.

However, receiving additional income from a death benefit, retirement account or HSA can change the amount of government benefits a person with special needs receives. Employees should consider consulting a legal advisor, and may consider creating a special-needs trust. Such trusts may help adequately protect beneficiaries over the long term.

When to review beneficiary designations

Selecting beneficiaries is not a one-and-done task but something employees should review regularly. You can also recommend that they update their beneficiary designations after major life events, including:

- Marriage or divorce

- Childbirth or adoption

- Loss of a loved one

By reviewing their designations, employees can help ensure their life insurance, retirement accounts, and HSA beneficiary selections align with their wishes and reflect their current family circumstances. These assets are an essential part of employees’ financial lives and can provide invaluable support in the event of a death.

Putting it all together: For employees, getting their legal advisor involved early is important to ensure that their will, estate plan, and beneficiary designations are well-matched, otherwise there may be unintended consequences.

Share The Dos and Don’ts of Naming a Beneficiary link with your employees so they can better understand the importance of naming beneficiaries, and pass benefits to their loved ones when they may need them most.

1 Triple-I Insurance Facts, Insurance Information Institute, accessed March 28, 2024.

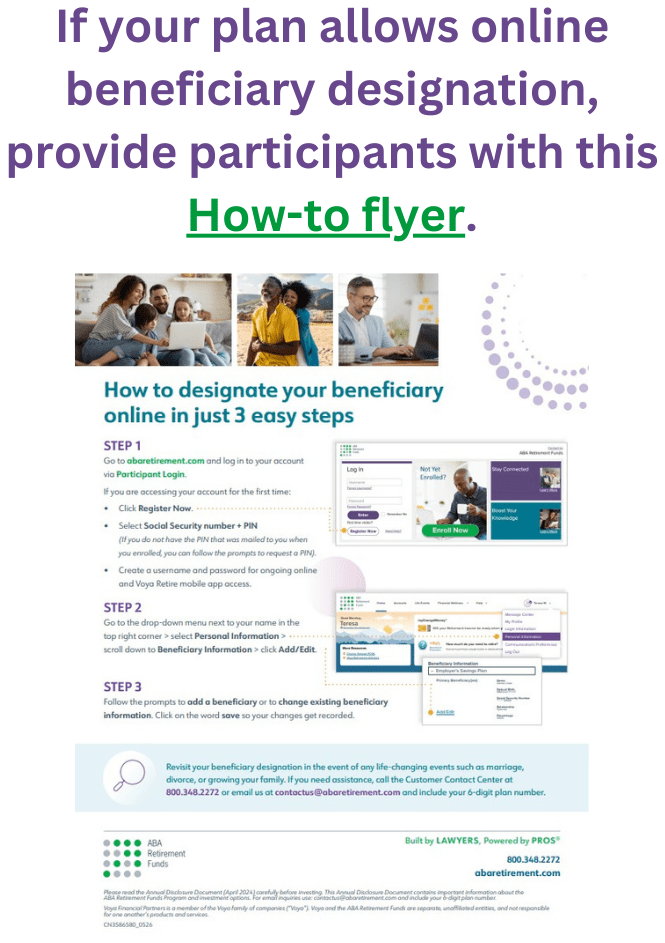

Note: If a participant’s account in your plan in the ABA Retirement Funds Program is already designated as a beneficiary account or alternate payee account, plan rules do not permit them to name their own beneficiary. If assets remain in a beneficiary or alternate payee account, the assets can only be paid to that person’s estate upon death.

Voya and the ABA Retirement Funds are separate, unaffiliated entities, and not responsible for one another’s products and services.

Please read the Program Annual Disclosure Document (April 2024) carefully before investing. This Disclosure Document contains important information about the Program and investment options. Contact us at: contactus@abaretirement.com.

CN3586756_0526