In-Service Withdrawals

See this page of the online guide for the six pre-approved reasons for taking a hardship withdrawal. The firm will need to determine which documentation to require to approve the hardship withdrawal, and maintain it on file in the event the plan is audited.

Please see section 14 of your adoption agreement to determine the in-service withdrawal provisions that your firm chose for the plan.

For an in-service withdrawal, participants should use the In-Service Withdrawal Form. If the participant has terminated employment or meets one of the other reasons for the request in section 3 of the form, use the Distribution Request Form. On either form, rollover instructions can be entered in section 8.

When someone’s employment status changes, notify the Program by submitting a Participant Data Change Form. The Program will send the participant a postcard the following year notifying them of their distribution options by directing them to this webpage. Participants whose vested account balance is $5,000 or less cannot continue to maintain their account in your plan; the Program will notify them that their account will be included in the annual “cash out of small account” sweep if they take no action within 90 days of the notice.

The Program can confirm for you if we have a beneficiary designation on file. Once beneficiaries are determined, each claimant should submit a Death Benefits Claim Form (for multiple beneficiaries, all forms should be submitted together). The Program will also need one certified copy of the death certificate.

In-Service Withdrawals

This section contains information on how to process participant in-service withdrawals. As Plan Administrator, you may handle the following types of participant withdrawal requests:

- Age-based withdrawals while still employed (generally, at least age 59½ or at retirement age as specified in the adoption agreement),

- Service-based withdrawals while still employed if allowed by your plan (certain service-based withdrawals require at least five years of participation in your plan),

- After-tax or rollover account withdrawals while still employed, and

- Qualified reservist distributions.

You will first need to determine if the participant meets the requirements for a withdrawal under the plan. You can do this by checking Article 7 of the plan document, as well as your plan’s adoption agreement.

Steps to request an in-service withdrawal

1. Determine if participant is eligible to request an in-service withdrawal; if so, send the In-Service Withdrawal Form along with a “Special Tax Notice Regarding Plan Payments,” “Notice of Benefit Payments,” and “Notice of Waiver of Annuity and Election of Alternate Benefit Payment Form” to participant

2. Decide what type of withdrawal to request and payment option

3. Complete and sign In-Service Withdrawal Form and send it to the Plan Administrator

4. Review, sign and send form to the Program

5. Process Form

6. Send check to participant

7. Send IRS Form 1099R to participant and IRS

Eligibility for in-service withdrawals

Generally, a participant is eligible for an in-service withdrawal from the plan if he or she has:

Met criteria for an age-based withdrawal and is still employed

At any time after reaching age 59½, participants may request a withdrawal from a profit sharing plan. With respect to a profit sharing plan (other than a SIMPLE 401(k) plan), withdrawals from accounts other than salary deferral 401(k) or Roth 401(k) may be available at an earlier age if permitted in the adoption agreement.

For a money purchase pension plan, an in-service withdrawal is permitted at normal retirement age (NRA). NRA is age 65 (or an age between age 62 and age 65 if specified in the adoption agreement).

Participants must specify the investment options and the amount or percentage to be taken from each option, unless the withdrawal is for the whole account. If no instructions are given, the withdrawal will be made pro-rata from all of the available options. Also, the amount is subject to any applicable withdrawal restrictions and taxes.

Met criteria for a service-based withdrawal and is still employed

If elected by the employer in the adoption agreement, a participant in a profit sharing plan (other than a SIMPLE 401(k) plan) may elect a withdrawal of the vested portion of employer contributions and employer matching contributions upon completing five years of participation in the plan.

Participants must specify the investment options and the amount or percentage to be taken from each option. If no instructions are given, the withdrawal will be made pro-rata from all of the available investment options. Also, the amount is subject to any applicable taxes, IRS early withdrawal penalties and withdrawal restrictions (for example, no withdrawals are allowed directly from the SDBA without first liquidating assets and transferring them to the Program’s investment options).

Met criteria for a contribution accumulation withdrawal and is still employed

If elected by the employer in the adoption agreement, a participant in a profit sharing plan (other than a SIMPLE 401(k) plan) may elect a withdrawal of the principal vested portion of employer contributions and employer matching contributions that have accumulated in the plan for at least two years.

Participants must specify the investment options and the amount or percentage to be taken from each option. If no instructions are given, the withdrawal will be made pro-rata from all of the available investment options. Also, the amount is subject to any applicable taxes, IRS early withdrawal penalties and withdrawal restrictions (for example, no withdrawals are allowed directly from the SDBA without first liquidating assets and transferring them to the Program’s investment options).

After-Tax Employee Contribution Account Withdrawal

If participants are contributing on an after-tax basis to a profit sharing plan, they may request after-tax withdrawals at any time. Withdrawals include the participant’s after-tax contributions and earnings, which are always 100% vested.

Participants must specify the investment options and the amount or percentage to be taken from each option, unless the withdrawal is for the entire after-tax account. If no instructions are given, the withdrawal will be made pro-rata from all of the available investment options. Also, the amount is subject to any applicable taxes, IRS early withdrawal penalties and withdrawal restrictions (for example, no withdrawals are allowed directly from the SDBA without first liquidating assets and transferring them to the Program’s investment options). Withdrawals will be made pro-rata from non-taxable contributions and taxable earnings.

Rollover Account Withdrawal

At any time, participants who have a rollover contribution source within their account (known as a “rollover account”) may request a rollover account withdrawal. Withdrawals include the participant’s rollover contributions and earnings, which are always 100% vested. Participants must specify the investment options and the amount or percentage to be taken from each option, unless the withdrawal is for the entire rollover account. If no instructions are given, the withdrawal will be made pro-rata from all of the available investment options. Also, the amount is subject to any applicable taxes, IRS early withdrawal penalties and withdrawal restrictions (for example, no withdrawals are allowed from the SDBA without first liquidating SDBA holdings and transferring the cash to the Program’s investment options).

Qualified Reservist Distribution

Participants who were ordered or called to active military duty after September 11, 2001, for at least 180 days (or for an indefinite period) may elect to receive a qualified distribution of their pre-tax 401(k) contributions and Roth 401(k) contributions while in active duty. Effective January 1, 2009, participants who are performing service in the uniformed services while on active duty for more than 30 days may request a withdrawal of all or any of their pre-tax 401(k) contributions and Roth 401(k) contributions while in active duty. Qualified reservist distributions are exempt from the 10% tax penalty on early distributions, but are subject to other applicable taxes.

Requesting an in-service withdrawal

If the participant is eligible for an in-service withdrawal, give him or her the In-Service Withdrawal Form along with a “Special Tax Notice Regarding Plan Payments,” “Notice of Benefit Payments,” and “Notice of Waiver of Annuity and Election of Alternate Benefit Payment Form.” If a participant in a money purchase pension plan wants an annuity payment, also give him or her the Annuity Quote/Purchase Form. If the participant wants to direct deposit the payment, also give him or her the Electronic Direct Deposit of Distributions Form.

To request an in-service withdrawal, participants must complete an In-Service Withdrawal Form. If the participant wants a quote for an annuity payment, he or she must first complete an Annuity Quote/Purchase Form. Then, upon purchase, the participant submits both the Annuity Quote/Purchase Form and In-Service Withdrawal Form. If the participant wants his or her withdrawal or installment payments to be directly deposited into his or her account at a bank or financial institution, the participant must complete an Electronic Direct Deposit of Distributions Form. If the participant wants a rollover distribution wired to his or her financial institution, the participant must complete a Wire Instructions for a Partial or Lump Sum Rollover Distribution Form.

If annuities are offered by your plan,* married participants who choose a form of benefit other than a “qualified joint and survivor annuity” must have their spouse’s signed consent. An Authorized Plan Representative or notary public must witness the spouse’s signature. The date of the witness’s signature must be the same date as the spouse’s signature. Both dates must be within 180 days of the withdrawal in order to be valid. Note: If the witness is a notary public, documentation must be provided (i.e., a raised seal or ink stamp). If the Plan Administrator is married to the participant, he or she cannot serve as the witness of the spouse’s signature.

*Available in money purchase pension plans and target benefit plans only, and profit sharing/401(k) plans with assets merged from a prior money purchase pension plan.

How to complete the In-Service Withdrawal Form (page 1)

- The plan administrator complete the employer information that relates to the plan.

- The participant completes the participant information.

- The plan administrator checks the reason for the request and completes the relevant information.

How to complete the In-Service Withdrawal Form (page 2)

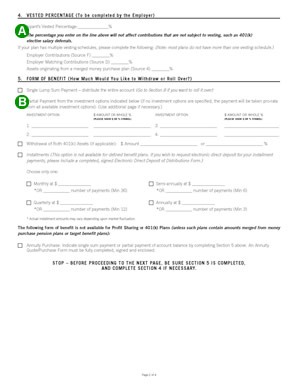

- The plan administrator completes the participant’s vested percentage. Bear in mind that your plan may have more than one vesting schedule for employer contributions — check your adoption agreement.

- The participant checks a form of benefit and completes the relevant information. Section 5 must be filled out even if the participant is requesting a rollover.

How to complete the In-Service Withdrawal Form (page 3)

- The participant should complete the Self-Directed Brokerage Account information, if applicable.

- The participant should read the required minimum distribution transfer restriction.

- The participant completes the direct rollover instructions, if applicable.

How to complete the In-Service Withdrawal Form (page 4)

- The participant must sign and date the Form.

- If the plan is subject to the QJSA regulations, the participant should review the information in the box at the top of the page and check the appropriate option. If the participant is married, spousal consent must be obtained and witnessed. Then, the participant sends the Form to the authorized plan representative for signature.

Sending the In-Service Withdrawal Form to the Program

Once you receive the participant’s completed In-Service Withdrawal Form, you must review and sign it as the Authorized Plan Representative. Then, submit the completed In-Service Withdrawal Form (and Electronic Direct Deposit of Distributions or Wire Instructions for Partial or Lump Sum Rollover Distribution Forms, if applicable) to the Program by mail or email.

The Program will process the In-Service Withdrawal Form in good order upon receipt. The Program will send a check (if applicable) to the participant.

Any distributions processed by the close of business on the last business day of the quarter will be reflected on the participant’s quarterly statement. Quarterly statements are mailed within 10 business days after the end of each quarter.

Unless there is a “direct rollover,” the Program will withhold 20% of the taxable portion of any distribution to a participant or beneficiary that is eligible for rollover. The plan must comply with any mandatory state income tax withholding rules (which vary by state). Participants will receive credit for payment of these taxes when they file their annual tax returns for the year in which the payment was made to the participant. Also, participants who want to elect additional withholding from the required minimum distribution payment may complete IRS Form W-4P at least 30 days before receiving the distribution. Form W-4P must accompany the distribution paperwork.

If benefits are distributed before age 59½, the payment may be subject to a 10% early distribution tax.

In general, participants who receive a check payable to themselves can roll over the full distribution amount to an IRA or another employer’s qualified plan within 60 days of their receipt of the check. However, to roll over the entire amount of the payment, the participant should (but is not required to) find other money to replace the 20% that was withheld for federal income tax. The participant receives credit for the taxes paid when he or she files his or her income tax return for that year. If the participant only rolls over the 80% that was received, the participant will still be taxed on the 20% that was withheld and not rolled over.

Amounts rolled over will not be taxed until the participant receives a payment from the IRA or other employer plan.

The participant may be able to use the special tax treatment for lump-sum distributions. The participant should see his or her tax advisor for more information. In January of the next calendar year, the Program will mail an IRS Form 1099-R to the participant regarding any taxable distributions for the prior tax year.