Portfolio Management

Mercer Trust Company’s portfolio management approach is ‘fit for client use’. For the Program, the use of multi-manager Fund construction is a key aspect.

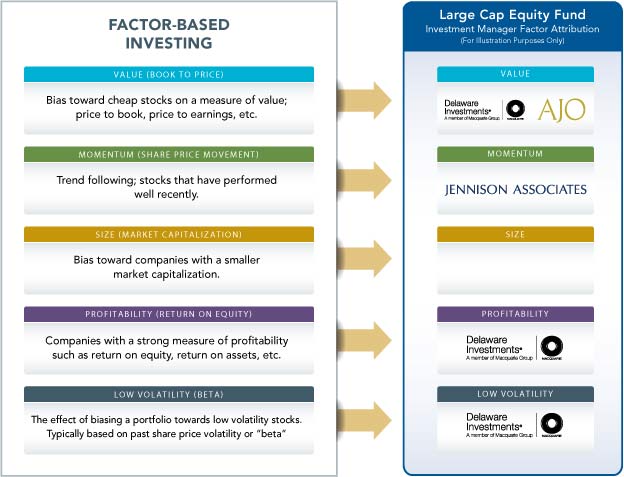

For the Program platform, Mercer Trust Company utilizes a multi-manager approach whereby a Fund’s assets are allocated to different investment managers, acting independently from the others based on their own investment style1. A factor-based investing portfolio management process is used to construct multimanager Funds. Factor-based investing allows for style diversification while focusing on managers and strategies that fit style factors that have historically proven to have generated positive returns over long periods of time2 (e.g., Value; Momentum; Size; Profitability; Low Volatility).

In addition to a multi-manager approach, Mercer Trust Company’s portfolio management focuses on the following aspects:

- Focus on high conviction: Mercer seeks to find active managers, which may at times own fewer names than their peers, and have lower turnover, which may improve investment performance as managers are better able to develop a thorough understanding of companies within their portfolios and factors that influence their long-term business values.

- Next generation managers: Mercer seeks to find managers that are well positioned to take advantage of the ever changing world of asset management, whether through technology, structure, human capital, etc.

- Risk/return characteristics: Mercer focuses on finding managers that are earning their returns for the appropriate level of risk in the portfolio.

- Innovative strategies: Mercer, through its global reach and thought leadership, seeks to identify new and innovative investment strategies to add value to its clients.

- Organizational fit: Mercer seeks to identify investment firms that diversify the client’s exposure by way of investment firms, and have strong and ethical practices that are in line with its clients.

- Generally Mercer Trust Company will use a multi-manager Fund structure; however, certain asset classes may not lend themselves to multi-manager solutions. As a result, each Fund will be separately analyzed to find the best investment solution.

- Magnitude of outperformance was in the range of 1% – 3% per annum (gross of transaction costs) over the last 20 years. Inception date for all return series is 10/31/1994; the ending date is 06/30/2014. Developed markets as defined by Style Research (matches MSCI). The factor portfolios are constructed by ranking the market of stocks by the respective factor scores, at each quarterly rebalance point the top 30% by capitalization of the ranked stocks is used. The portfolios are market cap weighted. Deciles analysis follows the same methodology but carves the universe into 10 portfolios of equal market cap size, based on a ranking against the given factor. All analysis is in USD and sourced from Mercer.

1 Generally Mercer Trust Company will use a multi-manager Fund structure; however, certain asset classes may not lend themselves to multi-manager solutions. As a result, each Fund will be separately analyzed to find the best investment solution.

2 Magnitude of outperformance was in the range of 1% – 3% per annum (gross of transaction costs) over the last 20 years. Inception date for all return series is 10/31/1994; the ending date is 06/30/2014. The factor portfolios are constructed by ranking the market of stocks by the respective factor scores, at each quarterly rebalance point the top 30% by capitalization of the ranked stocks is used. The portfolios are market cap weighted. All analysis is in USD and sourced from Mercer.